There’s no argument from the financial community that diversification isn’t needed in your long term investment strategy. The degree of diversification and how much diversification, however, is very much up for debate. We don’t think there will ever be a general consensus on this, and for good reason. Alternative Investment managers can’t even agree on how much investors should allocate to their slice of the pie, partially because you have to first determine what you want out of your diversification. Everyone wants something different out of their diversification and if someone tells you there’s a one size fits all approach, you can usually run the other way.

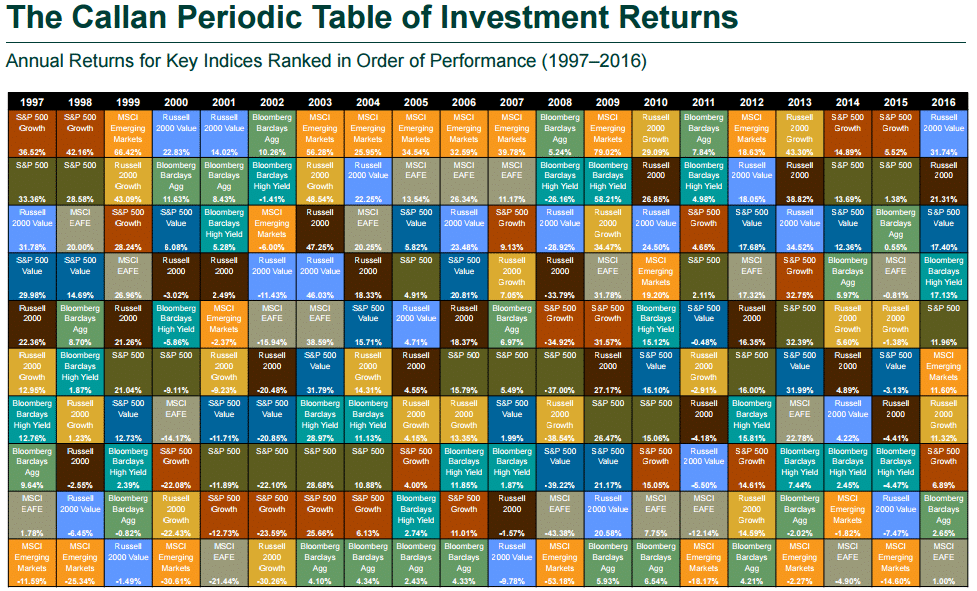

There’s no better evidence of the necessity of diversification than the Callan Periodic Table of Investment Returns that makes the rounds each year.

Or as Ben Carlson of “A Wealth of Common Sense Blog,” calls it, the asset class quilt.

It shouldn’t be shocking to know that we’ve discussed this chart multiple times (here and here). Our main issues are:

1) it doesn’t include Managed Futures / Global Macro – or really any other alternative investment. Here’s an ‘Alternative’ version that fixes that:

Large Cap = S&P 500

Small Cap = Russell 2000

Intl Stocks = MSCI EAFE

Emerging Markets = MSCI Emerging Markets

REIT = FTSE NAREIT All Equity Index

HG Bond = Barclay’s U.S. Aggregate Bond Index

HY Bond =BoAML US High Yield Master II

Cash= 3 Month T Bill Rate

Managed Futures = SG CTA Index

Hedge Funds = Hedge Fund Strategy QAI

Commodities =Bloomberg Commodity Index

AA = Asset Allocation Portfolio

(15% Large Cap, 15% Intl Stocks, 10% Small Cap, 10% Emerging Markets, 10% REIT, 40% HG Bond)

2) The periodic table/quilt doesn’t show the magnitude of the moves all that well (which really is the most important part of the chart in our opinion). Coming in fourth place in a year while also being down -36.4% doesn’t truly explain how much you’re really losing from your portfolio. So, we did another chart adding in the magnitude of the moves to reflect just how large some of those asset classes move year to year.

P.S. – Beware thinking the assets listed herein are all that’s needed to provide diversification. See 2002 and 2008 as prime examples of when asset classes became way more correlated than you might think. Just one of the topics in our whitepaper titled, “Why Alternatives.”

P.P.S – When big names in the financial world (Reformed Broker) tweet about commodities being bad over the past ten years.

It’s not an accident that commodities have been atrocious over the ten years ended 2016 considering their surge in popularity in 2004-2006. https://t.co/INEqkycleP

— Downtown Josh Brown (@ReformedBroker) March 20, 2017

And tables like these have commodities as the sole “alternative” asset in the chart, that’s a disservice to investors and the great diversification benefit of other alternatives; implying that alternatives can only make money when commodity prices are moving up. To that we say, uggh. Long only commodities are a bad idea, especially if accessed via ETFs. The truth of the matter is that there are 1000’s of systematic Managed Futures and Global Macro programs (register for our database here) that look to find returns when the futures markets move up and down.