Managed Futures, once an outsider in the financial space, sure seems like it is in the mainstream these days – a full 8 years after the financial crisis. Sure, the industry might still get criticized for “pushing the markets,” or poor performance over the last couple of years, but it’s not stopping big names like AQR from raising assets, and other large firms as seeing the asset class acceptable enough to open up their own ETFs.

Enter none other than JP Morgan, who just this week announced they are launching two alternatives ETFs; one of them with the uniquely unoriginal name “JP Morgan Managed Futures ETF.” It wasn’t so long ago, that many on Wall Street associated these non-equity trading programs as competitors. But now it’s the latest idea coming from one of the biggest banks in the biz, joining a handful of other ETFs and about 120 mutual funds under Morningstar’s Managed Futures Category. Yes, Chicago’s futures brainchild has become very New Yorkitized… with Wall Street product being created over and over again to get a foothold in the space.

ETFs

ETFs hold roughly $4 Trillion in assets worldwide, so it’s a little surprising to us there haven’t been more managed futures ETFs launched to date. But it isn’t an easy proposition, with the first mover and winner take all advantages present in the ETF space that discourage new entrants, as well as structural ETF issues which make accessing a managed futures return profile more difficult than say, the $GLD ETF which just holds Gold in a vault. Market makers, for example, need to have a deep understanding of the model in order to properly make a market for the ETF, without which you’ll have very wide spreads and nobody willing to pay an arm and a leg for getting into and out of the ETF. Here’s the list of the top ‘managed futures’ ETFs via ETFdb.com, but upon closer inspection, you can see only two of them have are actually doing Managed Futures. The rest is dedicated to a subset of the managed futures space – VIX and volatility strategies.

The leader in terms of assets is the Wisdom Tree Managed Futures ETF, which has been around for a while – enough for us to have gone under the hood of WDTI a couple of years ago – only to find it had some issues (like not being able to go short Crude Oil). We’ll see if the First Trust and now JP Morgan products have any better success, but it’s hard to get much more than average performance when designing the product to be a sort of managed futures index.

Managed Futures Volatility Strategies

A quick note on those other ETFs – What we find incredibly interesting is that these VIX and volatility strategies are categorized as Managed Futures ETFs from ETFdb.com. VIX and Volatility products have been exploding in popularity much like other alternative investment products since the end of the recent financial crisis, now totaling roughly $4 Billion in AUM. But volatility trading in the Managed Futures space has come into the spotlight recently, as its own sub sector. There are private funds with algorithms specifically dedicated to trading volatility markets. This is just the tip of the iceberg when it comes to learning about volatility related products. To learn more about this sub-sector space, download our “Investing in VIX and Volatility” whitepaper.

Managed Futures Mutual Funds

Meanwhile, over in mutual fund world, there’s plenty of packaged Managed Futures funds to go around. So much so, that we recently reformatted our Managed Futures Rankings to include top Managed Futures Mutual Funds. If you pop on over to Morningstar, they have 120 funds under their Managed Futures classification, but we find that is an overly broad categorization and is more of an overall alternative investment/futures using mutual fund category than a pure Managed Futures Category. As we discuss in our whitepaper, “Why Alternative Investments,” some alternative mutual funds (so called Liquid Alts) provide actual crisis period performance and non correlation to equity markets, while some are alternative in name only. It’s a tricky space to educate yourself about, with the categorizations across different platforms a spaghetti dinner of dozens of strategies out there – each with their own sub-categories.

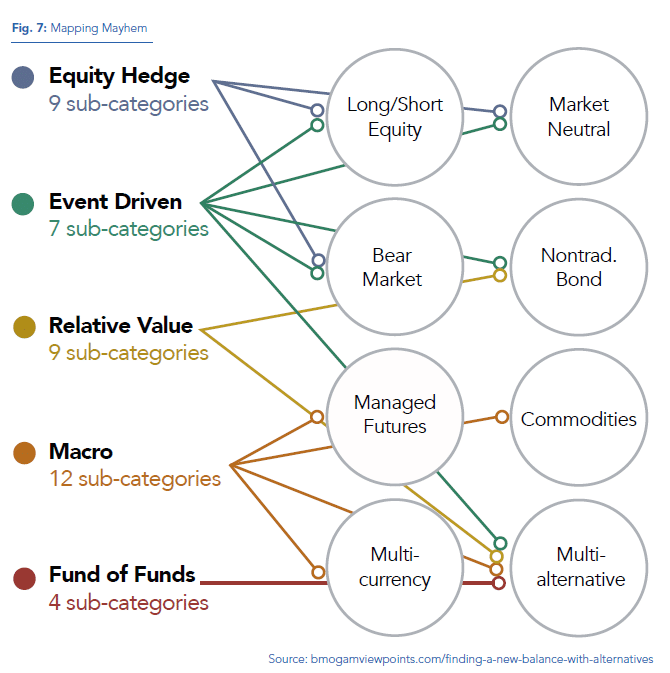

Here’s BMO’s Global Asset management on this problem:

“Distinguishing among strategies and identifying their sources of return and risk is challenging. The categorization of alternative strategies can be confusing. Hedge Fund Research lists four broad categories and 37 subcategories (plus four types of fund of funds); these do not always square with Morningstar’s system of categories (see Figure 7 on the next page). Investors may not know what they’re getting.”

We like to think it’s better to distinguish these sorts of alternative investments based on their correlation to one another and to the rest of your portfolio, rather than arguing over classifications that most will never agree on. But one thing we can all agree on, it seems, is that “Managed Futures” is now mainstream, having permeated the mutual fund, and now, ETF space. But if that investor base can understand what they’re really getting out of these products, and is educated enough to be able to endure the inevitable flat to down periods while waiting for the outlier moves which drive managed futures performance….remains to be seen.