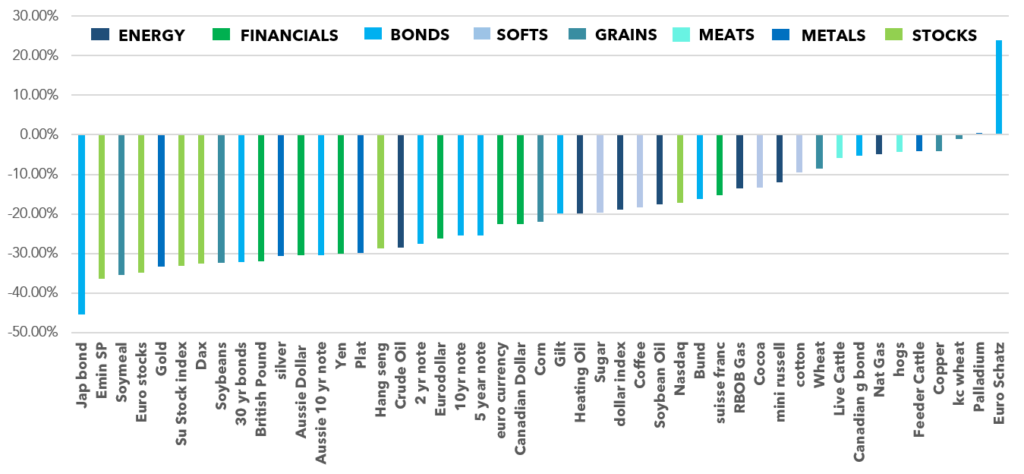

What is to come for Managed Futures in 2018? Hot off the keyword-presses, we have published our annual Managed Futures / Global Macro Outlook (download here). But before we get to 2018, we must look at that conditions that have paved the way to where we are now. 2017 will go down as one of the least volatile years in the futures markets in recent history, with just two of the 47 markets we track experiencing volatility expansion year over year: The Euro Schatz and a small expansion from Platinum. There are lots of ways to look at volatility, but suffice to say it wasn’t just the VIX at record lows – it was a contagion (or golden opportunity) across asset classes.

Volatility Expansion / Contraction

Across 47 Futures Markets

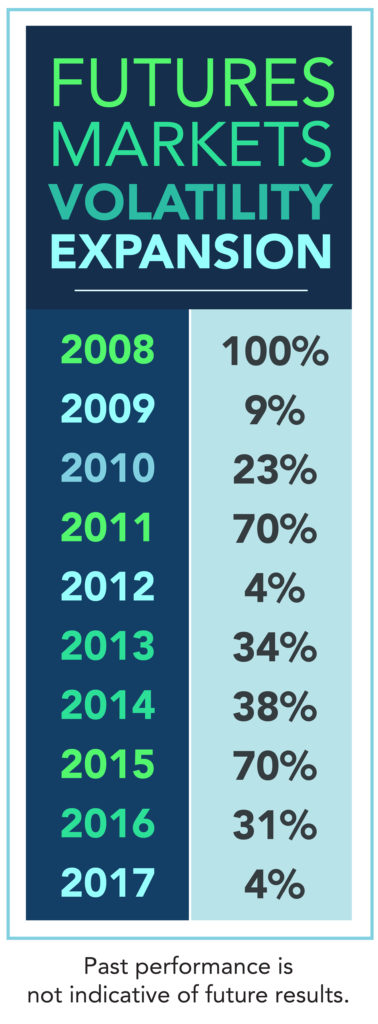

Here’s how this year’s contraction looks alongside the past several years in terms of volatility expansion/contraction:

So what will 2018 look like? Another act of low vol theater, or a new show highlighting yesteryear’s stars – volatility. Turns out, it isn’t as simple as hoping for some volatility expansion to fuel managed futures/global macro gains in 2018. By our estimation, there’s more short vol exposure within the assets class than ever before, whether it be outright volatility traders under the managed futures umbrella, or tried and true positive skew managers being tempted by the dark side of negative skew and short vol strategies over the past 5 years. We’ve already seen an uptick in volatility in currencies, and now stocks as managed futures has started off January with a bang.

What does this early success mean for the rest of 2018? Our Annual Outlook covers 5 scenarios that might help Managed Futures & Macro type strategies and 4 scenarios that could hurt; looking at the downtrend in bonds, a never ending bid for FANG stocks, a continuing flow of money into short VIX strategies, and how Bitcoin and ICO’s will change the futures markets and more.

To read our 2018 Managed Futures / Global Macro Outlook, access it here.