Many have questioned what the future holds for the hedge fund industry, given its history of innovation. What kind of products will hedge fund firms offer to their new investor? How will they reconcile profits with social responsibility? Will hedge fund firms even exist in the future, or will they have been replaced by artificial intelligence systems? If they do still exist and are still staffed with humans rather than machines, how will hedge firms navigate the coming generational change in leadership?

Luckily enough, most of those questions are answered in the Alternative Investment Management Association (AIMA) nice piece explaining the future of the hedge fund industry through the eyes of some of the titans of the space, such as Phillippe Jordan, Luke Ellis, and Ken Tropin. Here is what we found most interesting from the report.

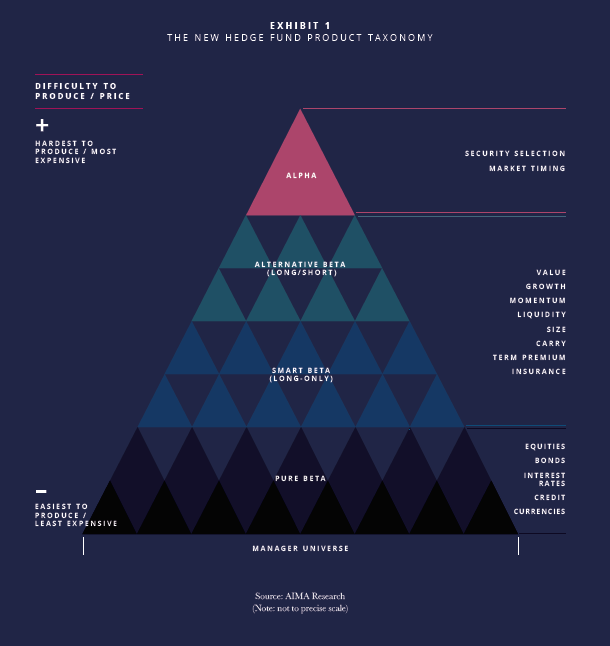

Alpha is Real but Rare

Smart beta and Alternative Beta look for continued expansion into these low-cost vehicles by hedge fund firms. Alpha is real but rare – and moving to a compressed time scale (edges lasting shorter and shorter). Given the skill needed to produce Alpha, investors will continue paying a premium (ie higher fees) to those who can deliver it.

Leda Braga of Systematica sums this up nicely:

A majority of investable assets in the total hedge fund pot will go to some form of risk premium investment strategy or a low-to-average correlation type of investment product, because investors have become increasingly more technical and have caught on to the fact that some investment strategies can be replicated for lower fees.

Going forward, I expect more than half of the hedge fund investable universe will comprise of the top ten largest investment strategies being commoditised into more low-cost investment products—the so-called liquid alternatives. The remainder of the universe will comprise of high-end niche investment strategies that are capacity constrained, and are able to deliver true alpha.

While AIMA has a nice food pyramid of sorts explaining the fee/skill landscape.

Quants and the Growth of Data

Firms are becoming more and more Quant focused while competing alongside companies like Google for talent. As we’ve mentioned before, Artificial Intelligence and Machine Learning will continue to be a large part of the hedge fund space.

The need for this quant talent is derived from the exponential growth in global data. Tom Hill of Blackstone says Forward-thinking hedge funds are structuring their firms in terms of technology and staffing to be able to analyze and harvest that data.

There’s an arms race around how asset management firms collect data and how they slice and dice it. Datasets purchased from third parties can degrade very quickly, so some funds are creating proprietary datasets that include everything from utilising cargo ship transporter data to monitor commodity flows, to using cell phone data to monitor retail foot traffic. The diversity of signals that quants are able to create has increased significantly.

Conscience Focused Investments

It’s not enough, anymore, to just post great returns. Frick from Unigestion says investors want it done responsibly – reflecting institutional investor values concerning the environment, social issues, and more.

There are already around 1,500 signatories—including asset owners and managers—to the United Nations-backed Principles for Responsible Investment. These principles encourage asset managers to act as stewards of the corporate landscape, and have brought about considerable improvement in companies’ corporate governance through proxy voting by asset managers and their engagement processes to improve corporate behaviour.

But a more conscience investment will have end return consequences. Phillipe Jordan of CFM says there will have to be a moment where investors look in the mirror and say they are willing to possibly accept fewer returns for that responsible profile:

We have taken a look at ESG factors and to date have not found any evidence that E and S are accretive to portfolio returns. That is not to say they are not valuable principles in the wider context of our complex societies and ecosystems, but there is no evidence to date that they contribute positively to increased portfolio returns or decrease risk.

Sold Not Bought

Securities Hedge Funds are sold, not bought… Distribution will continue to be a big part of the puzzle for hedge fund firm success. Competition is fierce; it’s not enough to just build it for investors to come. Just as much much thought and effort must be given to creating a true asset management firm with an eye towards distribution amongst retail clients. Here’s the AIMA report peering into the future of retail distribution:

Without changing their distribution models, hedge fund firms are less likely to be able to win retail business. To position themselves to do so they will need to embrace digital and mobile technology in order to engage a wider investor audience. Doing so will allow them to have the scalability, accessibility, and transparency retail investors expect, as well as the opportunity to service those investors at a much lower cost than has historically been possible. This technology will also offer hedge fund firms the opportunity to better understand an investor’s preferences, measure the sales effectiveness of investment solutions, and help tailor products to address different investor appetites.

For now, it looks like the future of the hedge fund industry looks to be full of liquid alternatives, quants, responsible investments, and new distribution channels. If you wish to read the full 108-page report, you can download it here.