Artificial Intelligence, Algorithms, Quants, Computer Driven Strategies, FinTech. No matter how you phrase it, those buzz words are here to stay in the financial realm. And what stories they have become… with yesterday’s more “normal” quant stories of machines taking over for analysts turning into stories about hedge fund managers trying to teach computers to copy their brain.

It’s no surprise there’s an uptick in press around these topics, with retail and institutional investors alike pouring money into the ‘quant’ space. If you follow the money, it’s easy to easy why this space is not only growing, but getting so much attention. Here are the eye-popping stats on the billions going into the space via Wired:

Quantitative funds have experienced significant growth. Investors are pulling away from traditional funds with human-led strategies, but there is more investment in quantitative funds. There was $38 billion of institutional investment into algorithmically driven hedge funds in the first quarter of 2016 alone. In October 2016, one of the biggest players, Renaissance Technologies, which has $60 billion under management, announced that it received $7 billion in investment the previous year.

But we still think the scope around the discussion of quants is far too small. What we find interesting isn’t classifying the money flows into quant strategies, but discussing what people are doing in the quant space overall; who and how algorithms are being built; where the lines blur with FinTech; and the lineup of players in the space. Sure, there are the big banks expanding their quant departments with recent grads with PhDs and degrees in computational finance (that’s an engineering degree if you’re all wondering); but in this consumer driven economy, it’s not just them and big hedge funds rushing into the quant world. Mom and pop investors are taking an interest, as are aspiring computer programmers and coders.

Not everyone can work in the quant department at Goldman Sachs, so the entrepreneurial spirit has taken hold – with everything from:

– American Idol-type crowd sourced quant modelling platforms where the winners get a big contract, to

– sort of Algo App Stores where investors can pick algorithmic trading strategies to be traded automatically for their accounts, to

– robo advisors (yes, those are quanty algos driving them), to

– the boring old systematic hedge fund traders in the futures space (read: managed futures) who’ve being doing this for decades

Yes, there’s a lot happening under the ‘quant/algo/fintech’ umbrella, so let’s break down just a few parts of it as seen in the futures world as best we can:

American Idol (ish) Crowdfunding Quant Platforms:

A couple months back, RCM’s Managing Director (and editor of this blog) Jeff Malec sat down with a handful of UCLA grad students in the Anderson School of Management Masters in Financial Engineering program, with the message – be more than just a quant. Having a quant on staff and building algorithms are really just the table stakes or price of admission these days. Those getting jobs and seeing their models in portfolios are the ones who also have some social skills and a bit of the entrepreneurial spirit. As we’ve talked about in previous quant posts, there’s sort of an arms race for quant talent to help build the next generation of algos and machine learning and what not, and the entrepreneurial sort is embracing modern technology to make sure they stand out from the crowd. They’re heading to one of many quant platforms which let all of the talent compete against each other for the rights to have their models traded with real money! Just like Shark Tank investing in an idea or the American Idol winner getting a record deal – except happening far, far away from the cameras, and instead of being waged on server racks.

Here’s a nifty chart of some of the bigger players via Wired, and links to their sites for your convenience: Cloud9, Quantopian, Numerai, Quantiacs.

The idea is that with more and more people able (both from a talent perspective and prevalence of the needed technology perspective) to build market trading algorithms, it’s much easier to have the quants come to you with their ideas than taking the risk of bringing in a couple into your department and hoping for the best. Here’s one example of a developer being attracted to these DIY Quant companies.

Towards the end of 2014, Nagai encountered Quantopian, a Boston-based company that enables so-called retail traders – private individuals rather than institutions – to build, test and submit trading algorithms of their own invention. To submit an algorithm, it was necessary to understand the common programming language Python. Nagai set about learning and, within a month, had submitted his first algorithm. Since then, he has submitted around a dozen, coming second in the Quantopian Open on one occasion with an algorithm that had a healthy 16.87 per cent annual return.

Although he doesn’t think it will happen soon, Nagai’s long-term aim is to be able to live well on the profits. He’s confident that his continuing study of the strategies pursued by the experts will pay dividends. “If you can study it, you can apply it,” he explains.

It gives these developers the opportunity to let the money speak for themselves (and making money off it), rather than cold calling hedge funds hoping to get a position, and for some, provide just as good (if not better) tools than they would be working on at a hedge fund or bank, developing the models. Here’s Quantopian’s CEO, John Fawcett:

“We have an interface and if you write to our spec, we can test it. We can trade it with your account and we can license it from you and trade it with our account. Providing that standardisation increases people’s productivity and opens up opportunities for them.”

Fawcett stresses that users who have submitted more than 400,000 algorithms retain copyright over their material. ”

According to Fawcett, Quantopian has 100,000 users in 180 countries and claims Quantopian is “institutional quality”. The institution is, effectively, in the browser. “If quants look at it and feel that it’s as good, if not better than the tool set they have internally, that platform has really been the beacon to attract our community,” he says.”

These cloud sourced platforms are allowing mass algorithm creation at a far greater pace, and far smaller cost – than the groups setting them up would otherwise have access to. The question now is whether there will be a winner take all effect here like in the rest of the tech space (see Apple, Google, Amazon), or whether each hedge fund wishing to crowd source algo creation will need to build out a similar platform. Our guess is you’ll see a little bit of both, with these early adapters becoming the main players – but other large hedge funds creating smaller, focused ‘contests’ via such platforms to meet certain specific needs. The big threat to these types of platforms is the technology itself. How far are we from AI platforms which can create millions of algorithms from which the hedge funds can select, removing the aspiring human quant from the equation. This is a fascinating space that bears watching.

Algo App Stores / Kayak.com for Quants

In the age of Uber, Instacart, and GrubHub, you have to bring the goods to the people. Why use recipes.com when you can get the food cooked and delivered to you. Along those lines, there are some groups that are bypassing the whole ‘build the algo’ part and offering up a menu of already built algos. We’re talking a slick interface for browsing through hundreds of already built algos and connections to the exchanges for live trading of them for your account. We liken it to an algo app store, where investors can link their brokerage accounts and turn on and off algos as they see fit, building portfolios of multiple algos, upping the number of contracts/shares traded, and so forth.

This is particularly appealing to the younger crowd who don’t want to take the time to make small talk with a broker, and that are used to well thought out interfaces, allowing them to do what they want (versus…say, filling out a form and faxing it in). And it seems the younger generation has no problem with trading futures and options – at least the ones that are financially savy enough to do that sort of thing, with derivatives trading becoming a bigger and bigger part of this plugged in 24/7 world, via Business Insider.

TD-Ameritrade Director of Trading Victor Jones doesn’t see mobile trading as the reason why more people are moving towards derivatives that aren’t tied to the 9:30 a.m. to 4 p.m. ET stock-market schedule.

More investors — millennial and older — understand they can use these instruments to manage portfolio risks, Jones said. Derivatives trading made up about 45% of TD Ameritrade’s transactions, he said, up from about 10% in 2009.

So the desire for derivatives is there, but how to access them in the most efficient manner? When your commute, credit card security, Amazon recommendations, and more are all served up via an algorithm, it’s only natural to think of algorithms for generating alpha in the derivatives space as well. The Algo store platforms show users trading algorithms like kayak.com shows you hotels or cars.com lets you browse new cars. All the stats are updated every day depending on market action – including the model’s backtested, forward tested, and stress tested performance.

But don’t take our word for it – check it out for yourself at one of the leading ‘Algo App Store’ sites: AutomatedTrading.com, which is one of many sites built using the iSystems backend technology.

Robo-Advisors (Quants in FinTech clothing)

But trading crude oil or gold futures on mobile isn’t for everyone – and neither is searching out a quant that meets your parameters. What about the people who don’t even want to go as far as finding the algo that’s right for them? Isn’t it just easier if someone picks it for you? Ask any millennial without a company 401k plan, and chances are they’re invested in a robo-advisor. It’s low cost and they handle pretty much everything else. Three years ago, we covered what was then a “disrupter” in the finance world, but now appears to be welcomed as part of the financial ecosystem. And while these companies are usually referred to as FinTech, the business model is based on some quant strategies for managing client’s money, applied in scale across 10s of thousands of the company clients. Gone are the days of your advisor giving you that stock recommendation on the golf course. Robo-Advisors have backtested, automated algorithms for investing clients money, rebalancing those investments, and even tax harvesting. They are ‘quants’ in innovator/fin tech/startup company clothing.

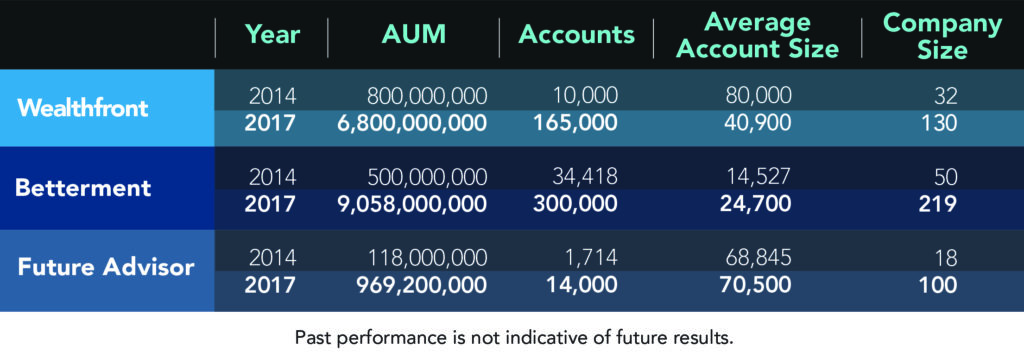

It’s a message that resonates well in our algorithm driven world. In our last look at the Robo-Advisors, we talked about how amazing it was that Wealthfront raised roughly $ 1 Billion in their first 30 months. Since then, they’ve raised another $6 Billion in the same time frame. Their competitor, Betterment, made up for lost time, is far ahead of Wealthfront on the AUM game, now holding $9 Billion in AUM. Here’s a breakdown of the business breakdown since we last talked about the robo-advisors:

Source: Brightscope

The most telling stat in this snapshot is the average account sizes: 40k, 24k, and 70k. We’re going to go out on a limb and say these are Millennials. This business model is using the quant or algorithm as a marketing opportunity for millennials to adjust investment ratios as they see fit with a simple slide on the screen without the small talk to their dad’s golf buddy (we know, that’s over the top cliché). Not to mention the low fees. The automated, machine driven algos don’t need to get paid or support a family or have a thirst for generating trades. That paired with the prevalence of low cost ETFs has allowed Robo-Advisors to greatly under cut their human counterparts in the fee department. They can ‘advise’ on thousands of clients simultaneously via the always on algos and a well-designed web interface allowing the clients to ‘meet’ with their advisor whenever they want.

Managed Futures/Systematic Global Macro (the so called Quant Hedge Funds)

Finally, we get to the group that’s being doing quant stuff before the word quant was even a thing. Futures focused hedge funds have been doing automated, model based, algorithmic trading for decades; using computers to crunch price data, generate signals, monitor risk levels, and exit trades. Some might even say they invented it. We’re talking quants who’ve have been trading currencies, grains, foreign bonds, WTI, going both long short these strategies making returns since the 1980’s. And it wasn’t just Ph.D. students in the back of a room. It’s people like Boston Red Sox Owner John W. Henry. For a little history on how these quants got started, we recommend reading our whitepaper on the history of Managed Futures.

These alternative investment managers combine all of the different aspects of the quant space together. They source their own quants to build the models (vs the crowdsourcing platforms above), hiring talented programmers and applied math types. They design their own infrastructure for testing the quant models, implementing them, and researching new ones (versus the Algo App Stores who’ve taken on this piece), and they do all of the risk management, portfolio creation, market selection, rebalancing, and so forth (versus the Robo-Advisors who automatically do this piece for investors). They are the top of the quant food chain, knowing and using each component part that FInTech companies have since broken out.

We’ve spent our entire career finding just these types of apex predators, researching what makes them tick and how they find alpha in the markets, as well as educating investors on how they act differently than your typical stock market investment. See here for more on that,or jump right to our database to find programs that match your risk and reward characteristics.

You’ll find big, well-known names like the following in the database:

AQR – You can’t go more than a few steps down the alternative investment sidewalk without running into AQR. They have successfully branded themselves as the go to quant hedge fund firm, and then offered all their products for low fees in a mutual fund format – which is now considered to be the benchmark for the rest of the industry (despite having recent issues).

Winton Capital – Winton is considered the largest managed futures fund (CTA) in the industry, even if CEO David Harding doesn’t consider them to be a CTA but rather a quant. We’ve interviewed Mr. Harding before on his success and his thoughts on some of the inherent issues of becoming the biggest CTA in the land.

QIM – Take a scroll through any of the Bloomberg articles on quants – and there’s a good chance you’ll see QIM in there somewhere (here, here, and here) . Back in 2014, their 3X leveraged program lost 34% — it’s worst drawdown in the program’s now 13-year history. The program followed up the very next year with a 72% return {Disclaimer: Past performance is not necessarily indicative of future results). QIM focuses on assembling 10,000 formulas through machine learning.

But there’s more to the quant space than just those stalwarts. There’s emerging manager talent, long standing success stories that pre-date the above names but haven’t had the same distribution (asset raising prowess), and niche strategies focusing on single sectors of the market. Here’s a list of names you might not know, but well worth checking out:

Goldenwise – GOLDENWISE is a quant based strategy focusing on volatility markets and recently won an award at the CME’s industry focused Pinnacle Awards for Best Emerging CTA. That’s right – here’s a strategy encapsulating two of the most popular themes in investing right now – volatility/VIX trading and quant models. Goldenwise seeks to profit from global macro trends, market inefficiency, and mis-pricings via VIX futures and other financial markets.

EMC – EMC’s is one of the original quants – from the days of the Turtle traders. But they’ve adapted to the times, while also launching three new investment programs after investing money in research and infrastructure. To learn more about EMC, download our research report on their beginnings and adaptation to the new quant world.

Auctos – Here’s a name you probably haven’t heard of, but they’ve been going head to head with AQR in the mutual fund world, and sort of winning recently (especially on the risk side). Auctos is a 100% systematic multi-system approach (read: quant) that seeks to capitalize on rising as well as declining price movements throughout the global financial and commodity markets. You can check out their mutual fund performance here: $ACXIX.

Jaguar – Jaguar’s quant strategy, AEGIR, adopts an algorithmic approach to exploiting price inefficiencies in the exchange-traded energy futures markets. The strategy is a forward-looking, dynamic investment model that evolves as the market evolves. To learn more about Jaguar, download our research report on Jaguar and their strategies.

So… will the Robots actually take over?

The biggest question is just how far can we go in this quant world? Are the days of the investment advisor in the corner office over? Or the discretionary global macro trader taking on the Bank of England on a hunch? Will it get to the point where there will only be 1-10 employees at quant firms because computers can do the rest? Will automation in the investment world have the same affect as other industries? Will these quants be able to provide better returns? Will we even need humans anymore?

Here are two quotes about the impact quants might have in the future:

“The time will come when no human investment manager will be able to beat the computer,”

– David Siegel, the co-founder of quantitative fund Two Sigma, which manages $35 billion, told an investment conference in 2015.

Models are a great place to begin, but not necessarily a good place to finish.” “It is a team effort and you need the analysts, traders and portfolio managers with the skills, experience and judgment to use and understand sophisticated financial models.”

– says Michael Hintze of CQS

There you have it. Whether it’s building algos, offering algos for use, replacing costly humans with algos, or managing billions of dollars in alternative investments via quant strategies – quants are here to stay. So much so, that the reference to automation, computerized trading, algos, and even ‘quants’ will likely fade into obscurity as that will just be how investments are done. The outlier will be whatever is opposite the quants in a few years time – where we might see articles talking about “human funds.”