A drive across farming states of the US has a different look than it did maybe 20 years ago, but we’re not talking about shopping malls having popped up where there used to be a farm. We’re talking about the drive from say Cleveland to Dallas seeing less and less wheat – those famous “amber waves of grain” – and more and more Corn and Soybeans.

How do we know? Well, while some of our Ag specialists have indeed been driving around the country meeting with farmers and checking out fields, but we’re getting the data from a recent Bloomberg piece with some great graphics.

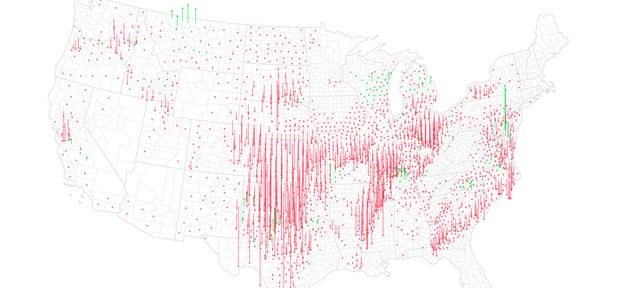

You can see the amount of wheat produced has fallen across the country, with just a few small green spots marking increased plantings here and there. The reason, according to RCM’s Director of Ag Services, Doug Bergman:

Farmers have gotten more efficient and better at switching plans to plant whatever best pays the bills. 10-15 years ago we started to see increased corn acres as the ethanol industry and subsidies to go along with it developed, while the last 5 years or so have seen more growth in soybean acres as Chinese demand (prior to the recent trade war) had been insatiable. And you have the large

Change in Wheat Production since 1995

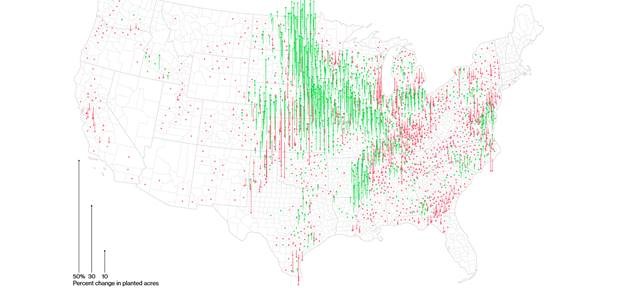

According to the Bloomberg piece – as global commodity markets have grown in the past two decades and growing economies like China have demanded more and more of US crops, the way farmers go about their business has also changed. The advancements in plant genetics and farm technology allow farmers to get more out of their land as well as decide what crop is best suited for their business plan. RCM’s Bergman adds that shorter season corn varieties have allowed the corn belt to move north while drought tolerant varieties have allowed it to move into more arid areas west. Sprinkle in a little help from Uncle Sam, and the result has been a massive increase in not just the amount of Soybeans and Corn planted, but where they are planted.

Change in Soybean Production since 1995

Change in Corn Production since 1995

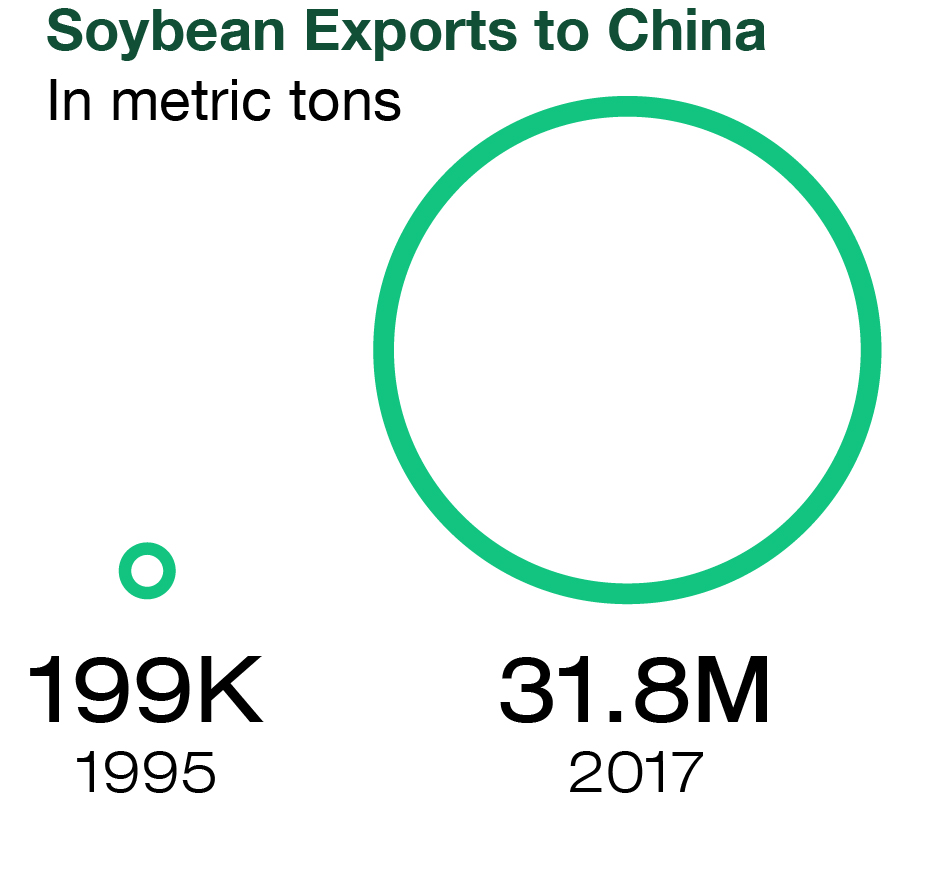

Here’s that China growth in Soybean demand, according to Bloomberg:

What will the future plantings look like? Maybe none, and we grow it all in the lab sci fi style. But more realistically, RCM’s Bergman sees depressed soy prices due to this year’s trade issues and a recent spike in global wheat prices likely leading to increased winter wheat planting by US producers this fall.

Either way, we may need to change the old amber waves of grain line to something about green fields of corn and soybean, as nothing 20 years in the making is going to change course all that fast.