While everyone is talking about the risks in China, with them ratcheting up stakes in the trade war with a Yuan devaluation, and threatening troops in Hong Kong to squash protests, many in the quant space are busy analyzing the Chinese markets for investment opportunities.

Now, we’re not talking about picking the next Tencent IPO (up some 2800% since inception) or betting on a China fueled commodity supercycle.

Jim Rogers was all over that investment way back in the early 2000s, and even penned a quick book when commodities were topping in 2007:

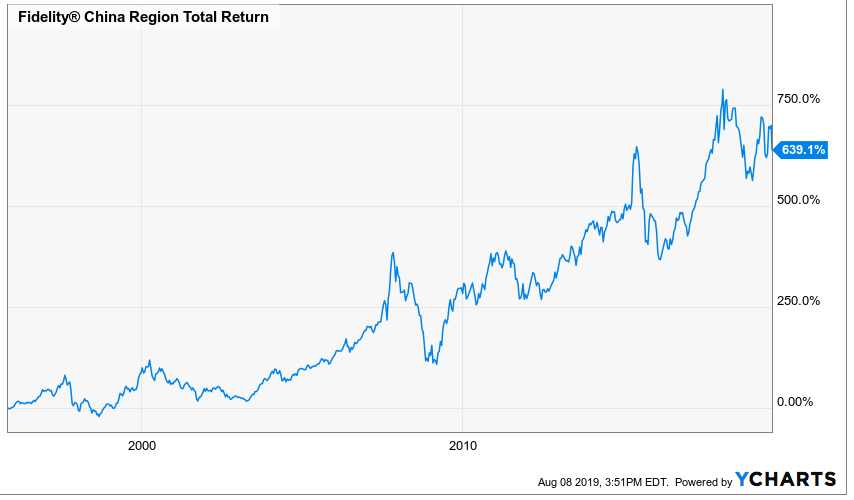

And as for investing in the China story via stocks in and around China – Singapore, Hong Kong, Korea, Japan, etc. – that game’s been around since before the dot.com bubble, with Fidelity having launched their China focused mutual fund way back in 1995.

No, the “China Story” is not a new one. They are huge, in terms of people, industry, commodity consumption, infrastructure needs, government securities purchases, military might, and more. Looking at China just for these reasons is old hat. Investors have been there, done that.

The Telegraph Road

Dire Straits classic Telegraph Road talks about the evolution of an economy (sort of), saying first came the churches, then then came the schools, then came the lawyers, then came the rules

then came the trains and the trucks with their load, and the dirty old track was the Telegraph Road, then came the mines, then came the ore, then there was the hard times, then there was a war.

Maybe its because of China’s Silk road initiative, but we can’t help but think of that song as we look at China today. First came the macro opportunities in the region as a whole, then the micro opportunities in the individual companies, then the commodity play, then the infrastructure, then the lawyers and the rules, for sure.

What’s the next ‘then’? Well, the more and more we visit the country to expand our efforts bringing western trading talent into the country to trade their nascent markets, the next wave as we see it is in the quantitative trading of the Chinese A-Shares market and their growing futures markets.

Long have systematic managers in the Western world complained of central bank intervention and the perceived artificial dampening of natural market volatility. There’s no such dampening of volatility in China, resulting in the good kind of volatility quantitative managers seek out. Quite simply, it’s easier to make $5 trading when the market is moving in a $20 range than it is to make $5 when the market only trades in a $7 range.

So, the next thing in China is similar to the next thing in the US back in the 80s, when systematic commodity trading advisors came on the scene not just investing in assets, but trading them back and forth, long and short.

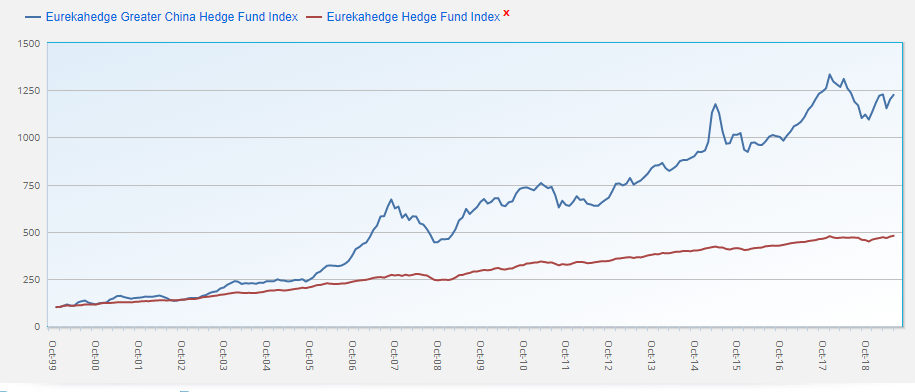

Consider the differences in Eurekahedge’s Chinese Hedge Fund Index and their overall hedge fund index to see just how much of a difference this greater volatility has meant for hedge funds in China as approaches have become more and more automated and quantitative over the last few years.

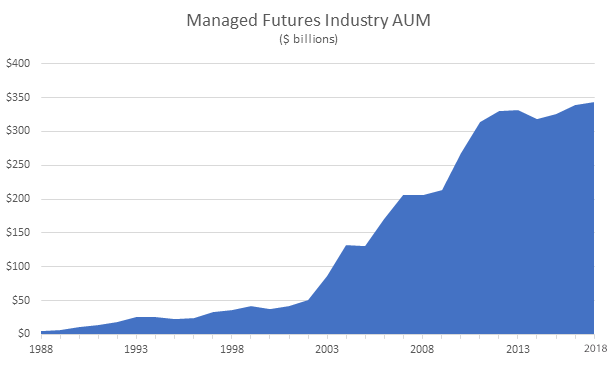

And now consider that the AUM of purely quantitative strategies being deployed in China is roughly in the single billions (as estimated by our Chinese partners). That about where US quant strategies (using managed futures AUM as a very rough proxy) were back in the 80s:

So, we’re going back in the time machine a little bit when looking at China, and finding the markets are behaving a bit more like 1980s/90s US markets with plenty of directional volatility from which quantitative approaches can capture significant moves, and not a ton of funds/assets competing for those same opportunities.

Who didn’t love the 80s? We’ll surely be hopping in our DeLorean with Marty McFly to see if we can find the next Mike Tyson of trading by testing how fast quants we find in China can solve a rubiks cube.

Coming back to the future and reality -we’ve already started applying our skills, team, and due diligence process to identifying talent with the access and connectivity to these volatility producing Chinese markets. The result, quants using AI to do long/short strategies with futures overlays. Quants analyzing futures curves on Chinese markets for spread trading opportunities, and classic volatility breakout type models which love the directional momentum.

Yes, the China story is old. Like, 1980s old. We’re fine with that. Long live the 80s!