After days of pushing higher and higher, is the down trend in the US Dollar over? Trend following type managed futures strategies sure hope that isn’t the case. They love them some trending US Dollar.

Most analysts, however, have looked for the dollar to remain under pressure after a steep slide last year, arguing that a global economic pickup and the Federal Reserve’s commitment to letting the economy run hot before pulling back on monetary stimulus would see the dollar slide versus major rivals. (MarketWatch)

It’s pretty obvious that there are a few factors affecting the shift in USD including the pending stimulus bill & Biden Blitz which is pretty similar to what we saw last stimmy season in August. We could be looking at another rise in prices just to see a sell off when Biden signs the bill:

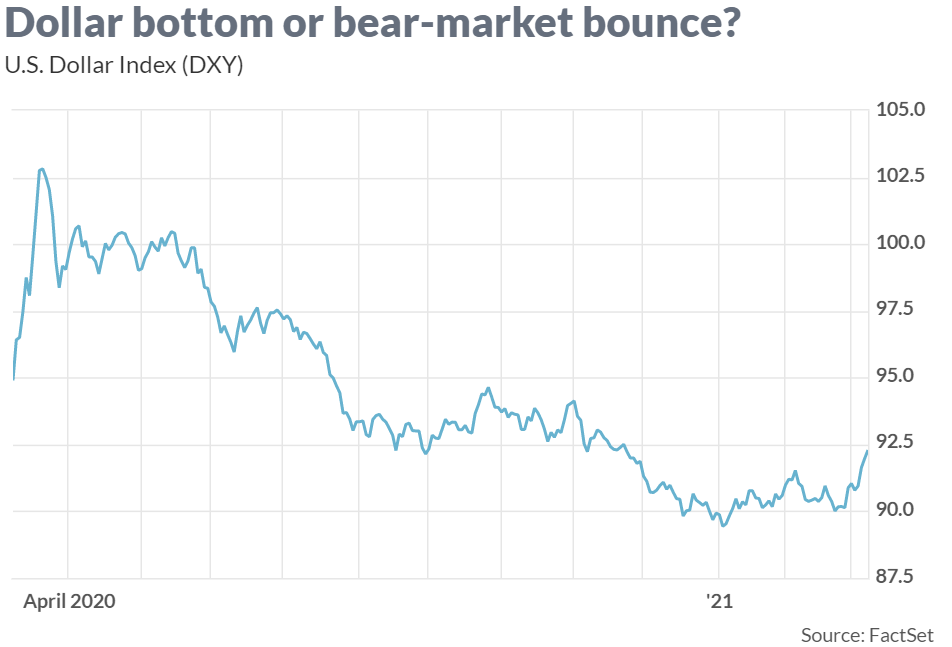

What do you get (besides a gold and silver rally) when you do $3 Trillion in stimulus, and the Euro countries find out they can do a coordinated monetary policy? A U.S. Dollar sell off! After spiking from around 98 up to 104 in the depths of the crisis, the U.S. Dollar has sold off rather heavily, falling down to 92 (as of our writing this, we have a knack for inadvertently calling a bottom as soon as we write up something about a market).

What’s happening? Well, if you’re scared that Trillions in stimulus makes runaway inflation a possibility, lessening the purchasing power of your fiat currency, you sell dollars and buy gold (or Silver, or Bitcoin). If you think the Eurozone has figured out how to all coexist and are stronger together than they are apart, you sell dollars to buy Euros, and so forth. The common denominator, is selling dollars. (RCM Alts)

The ”I word” of Inflation has been a big storyline so far in 2021, furthered by economists worrying about overheating due to another stimulus bill being passed. But in the world of Managed Futures – if we’re being frank, we’re over here chanting Bring It On nearly 7 months after the first time!

Traditionally, a rally in the Dollar Index has proven to be very beneficial for Managed Futures. That’s because it typically means the other currency markets are also moving with the same sort of depth. The other part of the reason managed futures tends to do well when the U.S. Dollar is trending, is because the U.S. Dollar index impacts almost all commodity futures markets simply because those markets are priced in the U.S. dollar. That means, for example, a falling U.S. Dollar can translate to rising prices in dollar denominated futures markets (all else being equal).

Here’s a look at the historical performance of Managed Futures (as measured by the SocGen CTA Index) has performed in different Dollar Index periods of strong trendiness, which we measured by the 14 day ADX indicator seeing values greater than 40, and then looking at the percentage of days the indicator saw such high readings each year. Here’s what we found. Managed Futures love it some strongly trending USD, with all but one year in which more than 35% of days were in strong trend seeing gains (90% of time), versus just 60% of the time when there weren’t as big of a percentage of strongly trending USD days. What’s more – the upsides were completely different, with the trending USD periods seeing a much higher ceiling for their performance (40% of the time with double digit years) versus 0% of the years seeing double digit gains when strong trends in the USD weren’t as frequent. All in all, in the strong US Dollar trending years, we saw a max of +15.25%, min of -2.87% and average year of 8.22%, versus a max of 6.26%, min of -5.83%, and average of just 0.42% in the other years.

So bring on that U.S. Dollar weakness. CTA’s will welcome it with open arms.

(RCM Alts)