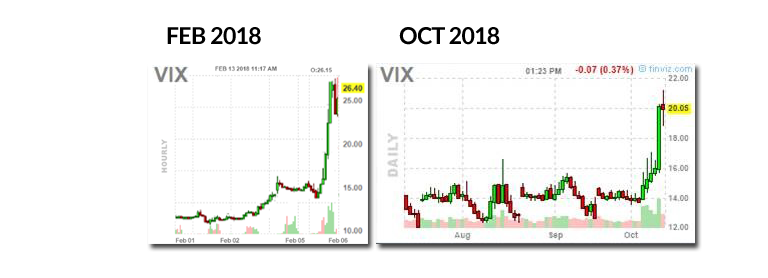

ok Maybe it was the Cat 4 hurricane barreling down on the Florida panhandle which had everyone’s attention, but yesterday’s VIX spike sure didn’t feel like the one that brought people out in body bags back in February. February 5th saw the Dow fall about 1,200 points, it’s worth point loss in history; while yesterday saw a decline of about 850 points, its third worst decline in history. Feb represented about a -10% loss from the highs. October here has seen a drop of about 6% from the highs (about -9% in the Nasdaq). Here’s both spikes in VIX futures via finviz.

So what gives? Why was February a spike of 116% (13 to 37) and October here a spike of only about 50% (14 to 21)? Well, for one, this move was smaller. In the non-linear world of derivatives on top of derivatives which is the VIX, a small difference can have a huge effect. This is the world of fat tails. Two, we did have February – which for all its destruction did prepare people for another day like it, perhaps meaning less of a knee jerk reaction. Finally, there wasn’t a multi-billion dollar ETF unwinding its trades this time around (we’re looking at your $XIV). For more on the move, we turned to Tim Jacobson of Pearl Capital, who caught the February move and has been analyzing this one with great interest:

Compared to Feb 5, this sell-off has not generated the same reaction in the VIX. To put it in perspective, Feb 5 had a sell-off of around 150pts in the E-mini S&P 500. The VIX Futures were up about 17pts. Yesterday, the approximate 100pt sell-off in the E-mini S&P 500 only prompted a 4pt move in the VIX Futures. This is a very normal reaction for follow-on volatility episodes. A similar moment was Aug 2015 and Jan 2016. In both months, the S&P 500 sold-off to similar levels but the VIX did not react as much in Jan 2016 as in the August episode. What is happening is the VIX usually stays muted unless or until the market makes a new low or the past volatility is far enough away that the market has reset. There is certainly enough concern with stress in China, rates, and valuations to combine for continued selling, but unless that happens, the VIX may not be as reactive to downward moves in the E-mini S&P 500 as we have seen earlier in the year.

One other point to highlight is the significant volumes we are seeing in the VIX Futures. Many had predicted that with the washout of VIX-related ETFs in February that VIX Futures volumes would be impaired going forward. We have not seen that to be the case. Volumes in VIX Futures products have remained strong prior to and through this most recent market sell-off.

Disclaimer:

This presentation was prepared for discussion purposes only. Pearl Capital Advisors, LLC (“Pearl”) disclaims any and all liability relating to this presentation and makes no express or implied representations or warranties concerning the accuracy or completeness of this presentation, the contents of which may change without notice. This material is not intended as an offer or solicitation for purchase or sale of any financial instrument. This presentation is not intended to provide, and should not be relied on, for tax, accounting, regulatory or financial advice. You should consult your own advisors. This presentation does not purport to describe all of the uses associated with financial transactions and should not be construed as advice to you. Past performance is not indicative of future results.

There you have it – direct from the horse’s mouth, and sort of hitting on our second point above, that a 2nd spike (even when separated by 8 months) tends to have a more muted reaction than the first spike. We’ll have to press them on exactly how long has to pass before a spike is considered a new one or a follow on move, but with the markets only having gotten back to basically where they were in February, we can see an argument for this being the same market environment, just removed some.

This isn’t our first rodeo when it comes to shedding some light on all things VIX and volatility. Here’s some highlights from the archives:

“INFOGRAPHIC: How to Trade the VIX”

That’s actually a trick headline, as you can’t trade the VIX directly. It’s just an index of options prices. But you can invest/trade in products that track the VIX, like VIX futures, VIX ETFs, inverse ETFs, and more. It’s called trading volatility, and with seemingly everyone giving it a shot of late (Billions are in VIX futures-related ETFs), we thought a nifty flowchart of just how to proceed would be worthwhile.

“WHITEPAPER: Investing in Volatilty & The VIX”

Nowadays, there are dozens of ways to get exposure to VIX and Volatility. Can you say you truly understand how these products work and the difference between the VIX and VIX Futures? We’ve put together a fundamental report to help investors understand the history of the VIX, how it is determined, and the many investment possibilities around the so called “fear index.”

The February Spike:

WHY DID XIV IMPLODE?

Ironically, the popularity of these products significantly increased the probability of their own demise. These products, and others like them, provided a simple vehicle for betting against volatility.

THE CHART SHOWING WHY THIS VIX MOVE IS UNIQUE

Enter February 5th, 2018 – where something curious happened – the fear gauge disconnected from actual fear in the market.

A VOLATILITY TRADER EXPLAINS WHAT HAPPENED

We’re no experts in VIX and volatility trading, but we did ask those that trade millions in VIX Futures to give us some insight.

THE TAIL HAS WAGGED THE DOG

When the dust settled, we’re now living in an environment where there’s nearly $4 Billion less short volatility supply than there was just a week ago, once you add in all the private funds that were also on this trade.

VIX TRADERS SEE FEB RETURNS FROM +30% TO -95%

Here is our completely unofficial listing of several volatility trading firms, via both VIX and index options, and how they have fared thus far in February – with the very big disclaimer that these aren’t official numbers from the managers

Oldies but Goodies:

“Scenes from “The New Asset Class: Investing in the VIX”

But while most of us are using the VIX as a metric to measure asset classes, others are treating it as a unique asset class in its own right, designing investment strategies around the futures and options which are tied to the CBOE’s VIX index.

Maybe it’s just us – but we don’t think a “wait-and-see” approach bodes all that well for a portfolio when it comes to volatility. It’s a little like trying to put on your seatbelt in the middle of the car crash.

“Seller Beware: Everybody’s Short VIX These Days”

The $4 Billion dollar questions are how crowded can this short volatility trade get before the dam breaks? And will it amplify any such breaking? We also wonder if there is a never ending supply of long volatility dupes, or if they will eventually wake up to the issue of giving up the 4,300% outlined by Goldman in their research? And at what point does the insurance become too costly to deploy day after day after day?

“INFOGRAPHIC: Honey, I Shrunk the VIX”

There’s been a growing chorus lately suggesting that perhaps the record low VIX readings aren’t due to record low feelings about volatility, but instead due to the dramatic increase in VIX products and assets betting on decreases in volatility.

“Pascal’s Wager – Trump/Kim Nuke Style”

We’ve talked in the past about Pascal’s Wager and simple decision matrices, and couldn’t help but think that today’s market rebound as the perfect example for why the VIX gets slammed off its spikes so frequently.