We’re closing out the decade with one final look back on some of the top performing markets, asset classes, and alternative investment funds over that time.

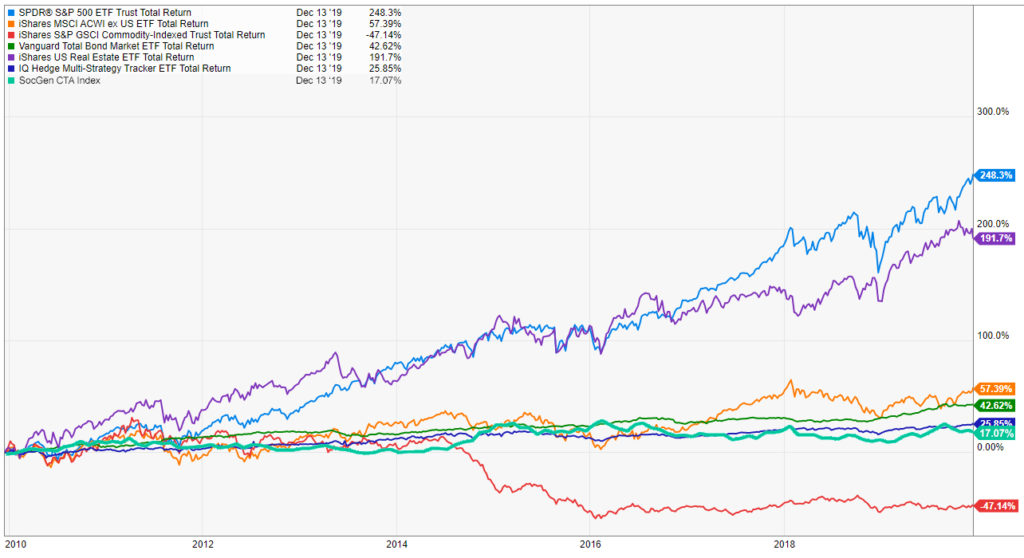

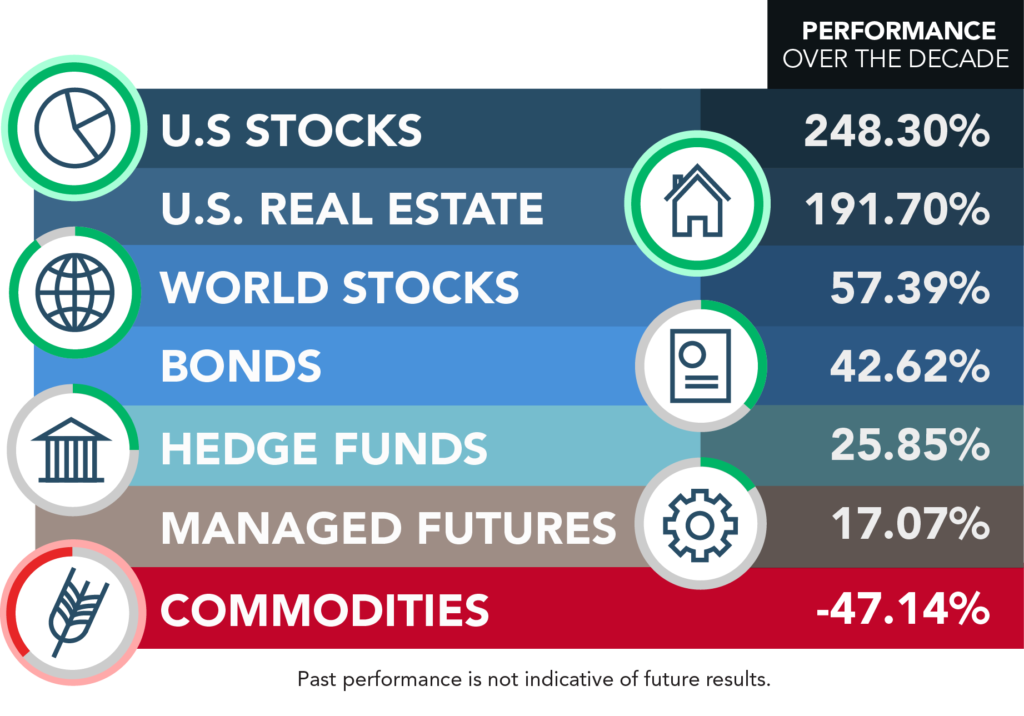

Last up, the broad asset classes we track in our monthly Asset Class Scoreboard: US Stocks, World Stocks, Hedge Funds, Real Estate, Bonds, Commodities and Managed Futures – where it was mostly a two horse race for the past 10 years between US Stocks and US real estate – with both taking on around 200% since Jan 2010. Wow, thanks Amazon (up about 1,200% for the decade). On the flip side was commodities, which had some notable decade long losers (see Commodity Performance Over the Decade (2009-2019)), plus a problem with a negative roll yield to end up roughly cut in half over the decade.

After that, a whole lot of mediocrity in international equities, bonds, and alternatives (hedge funds and managed futures), with each solidly in the black – but no where near the astronomical heights of the S&P 500. Bonds have to be the biggest surprise here, with the calls for rising interest rates and an end to the ultra-low rate environment persisting for most of the past 10 years – and bond markets ignoring all of it by still rallying to the point where we now have trillions in negative yielding debt! Can that continue for the next 10 years?? This severe underperformance by hedge funds will likely get people talking about the apples/oranges comparison of them lagging equity markets by so much (pro tip: investors don’t care, that’s not why they have hedge funds) – while the massive vacuuming out of volatility across the globe can perhaps nowhere be better seen than in long volatility focused manager futures and their decade long water treading amidst record low vol.

This was surely not the decade most professionals saw as a possibility sitting there on NYE of 2009 with the financial crisis fresh in their minds. The Black Swan nobody saw coming, it turns out – was the lack of any black swans. The old White Moose, as we’ve taken to calling it.

Asset class performance over the decade: