We used to track bond king Jeff Gundlach’s investment calls from time to time – see here and here, and didn’t miss a good Gundlach macguffin…especially when he’s talking our world of commodities.

Here’s Gundlach, via Markets Insider talking today’s environment in commodities:

“Commodities are unbelievably strong. But for the fact that they haven’t had any correction, I’d be wildly bullish on them. They are still quite cheap on a long-term basis versus the S&P 500. When the worm turns – which it looks like it has on commodities from a very cheap level – it’s not foolish to believe that commodities could outperform by several hundred percentage points.” – Gundlach suggested investors put 30% to 35% of their portfolio in commodities and other physical assets such as real estate and gold.

But 30 to 35% in “commodities and other assets like Gold?” As much as we love commodities, we’re not so sure that’s a good idea. Even if commodities are set to spout higher, they are known for their rather extremely volatile nature, as pointed out in this old post.

Over this nearly 25 year period, a diverse portfolio of commodities would have earned investors similar returns to cash with similar volatility to stocks, the exact opposite of what you would want to see from a long-term asset class. Factoring in inflation the real returns were 0.37% and 1.45% annually for the respective commodities indexes.

This data makes a strong case that commodities don’t make for a solid long-term investment as a dedicated allocation in a portfolio. They are probably much more conducive to trading than investing – Ben Carlson

Don’t be dismayed at the prospect of such poor risk-adjusted returns. Enter trend-following CTAs, or commodity trading advisors/managed futures – which are having a bit of a resurgence of late as many commodities maintain strong trends since their COVID lows last year.

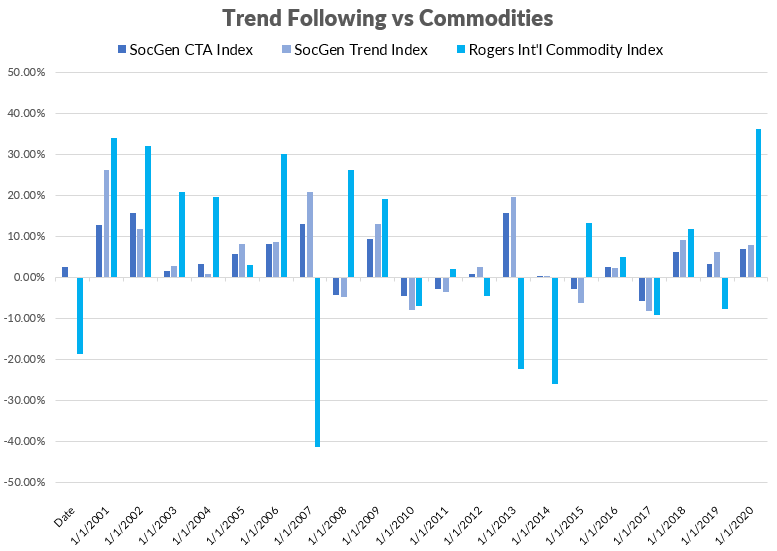

Sources: SocGen CTA Index, SocGen Trend Index, Rogers Int’l Commodity Index

Investors haven’t missed a beat, seeking out skilled commodity traders and even asking yours truly for some good resources on trend…

Trend-following strategies might be coming back in style, if inflation stays. Any recommendations on books, papers or resources? pic.twitter.com/rFXp5FHQB9

— Pablo Villalba (@micho) October 18, 2021

For podcasts, I’ll second @TopTradersLive. It’s excellent. @rcmAlts also has some fantastic guests discussing trend (Kaminksi, Crittenden, @AuspiceTim, and many others). And @JasonMutiny and @TaylorPearsonMe have some great guests on their pod.

— Nick (@Nicholas_Meyers) October 18, 2021

@Nicholas_Meyers provided an alley-oop for our very own podcast, The Derivative, which delivers in-depth chats with the best and brightest in the alternative investment world. Our pod offers the opportunity to listen to top hedge fund managers tell enchanting stories and dive into how their strategies work for attacking everything from commodities to crypto. Here’s five commodities and trend following pods you didn’t know you needed:

- Debunking Trend Following’s Dead Theories with Katy Kaminski

- BLNDX[ing] Trend Following and Global Equity with Standpoint’s Eric Crittenden

- Canadian Commodities and Building Business with Tim Pickering of Auspice Capital Advisors

- Weigh More than You Wanted to Know About Meat, with AgriTrend’s Simon Quilty

- Charting a Chinese Commodities Course with Fred Schutzman of Abingdon Global

We suggest taking a short trip through a few blog posts and our educational materials on Trend Following:

- Michael Covel’s book on trend following

- Here’s a Guy Managing $25 Billion with Trend Following

- 100 years of Trend Following

- Commodities and Non-Correlation

- The pic from space showing how commodities are non correlated

Our series on how a trend following trade works:

- Is this a down trend?

- Anatomy of a Trend Following Breakout – Crude Oil

- Crude Trends and Cursing your Manager

- Anatomy of a Trend Following Trade – the Short Side

- Anatomy of a Trend Following Trade – the Short Exit

- Anatomy of a Trend Following Trade – the Journey

And last, but certainly not least, don’t forget about commodity specialists who know their niche. Unlike other asset classes, many commodity markets have seasonal supply and demand forces. Combined with the potential for carry in the term structure, these markets provide opportunities for alpha with little correlation to anything else. Specialists who spend their carriers exploiting these opportunities are worth following.

- Red Rock Capital Commodity Long/Short

- Cazadores Investments Commodity Alpha

- Jaguar Investments AEGIR

- Opus Futures Advanced Ag

- Auspice Capital Advisors Auspice Diversified