When you think of commodity market performance, what’s one of the first things you think of? Positive or negative performance? For anyone who has invested over the past 10 years, the answer has been mostly negative… and even when it hasn’t been, commodity markets cyclical moves up and down tends to be at odds with the way the stock market moves (generally up and to the right). All of this is to say, commodity “exposure” in a portfolio has left a lot to be desired recently, with leading ETFs like $DBC down -45% and $GSG down -55% over the past three years (Disclaimer: past performance is not necessarily indicative of future results), and financial bloggers like Josh Brown taking their digs.

Commodities = more volatility than stocks, lower long-term return than cash. Brutal.

— Downtown Josh Brown (@ReformedBroker) July 24, 2017

Still, there are pockets of inverse single commodity ETFs out there (DWT, BOS, and ADZ) that have managed to make some money as the general commodity indices have struggled, riding down trends to profits. As the old saying goes, the trend is your friend, and perhaps nowhere more than in the commodities space, where some of the first quants turned analysis of price trends into systematic strategies for finding alpha (or as it’s called now, trend/momentum beta) on the up and down swings in dozens of markets. The problem is you’re not going to find commodity specific trend followers in the ETF space – at least not yet.

We may be giving up the idea for the next big ETF here, but we’ve been hammering the ‘long and wrong’ is bad in commodities drum for a while now. Maybe some other voices would help. Enter one of Ritholtz Wealth Management’s bullpen aces – Ben Carlson – who tackles this subject in his own unique way, outlining that trend following rules are the best way to gain meaningful exposure to the commodity markets. Props to Ben for putting trend following in the mainstream on Bloomberg.

Where we disagree, however, is where to apply the trend following rules. Carlson suggests – applying a simple strategy to an ETF that tracks companies that are involved in the commodity space. In this particular case, it’s the Vanguard Precious Metals & Mining Fund.

The basic idea is to ride the momentum up when they are rising and try to get out of the way when they are falling, with the understanding that you can’t nail the timing perfectly in either direction.

Our trend-following strategy in this example follows a simple 10-month moving average rule. Using the same Vanguard Precious Metals & Mining Fund, this strategy shows what would have happened if you would have held that fund when it was above its trailing 10-month moving average price and sold it to buy bonds whenever it dipped below the 10-month moving average.

Even though investing in a company that digs up commodities is a really bad idea (See here, here, and here) – even a generic option of going long and short that market proves to be better than just making money on the up swings.

Not only does a trend-following strategy cut the volatility by roughly one-third in this fund, but it also reduces the maximum drawdown in the fund from minus 76 percent to minus 33 percent by going to bonds as losses and volatility began to pile up.

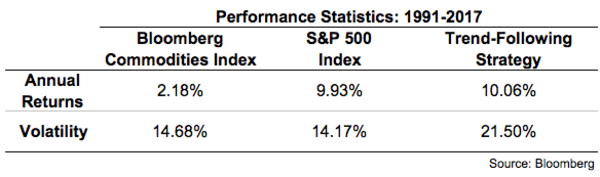

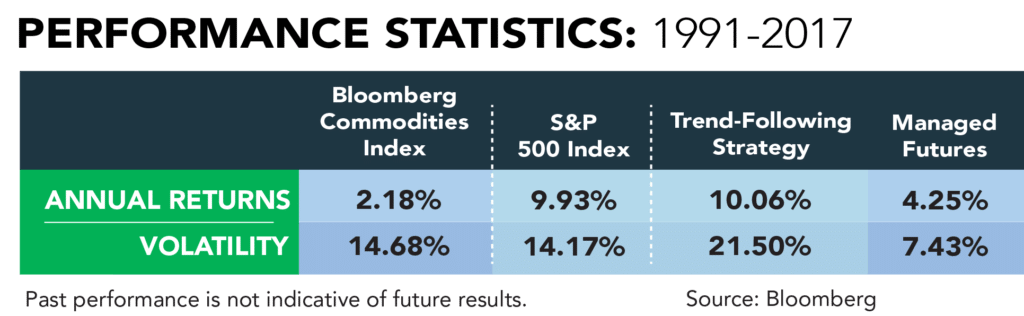

Cutting a drawdown by 37% is a big deal! But, in our humble opinion – people shouldn’t be gaining commodity exposure by accessing commodity companies. The best commodity exposure is from the commodity markets themselves – particularly the futures markets designed to hedge and speculate on commodity prices. And it just so happens there’s an entire asset class out there designed to do just this. Managed Futures, which at its simplest level applies trend following strategies to the commodity futures markets themselves. What happens when we put managed futures up there alongside commodities and Mr. Carlson’s trend following approach – we can see Managed Futures has the lowest risk of them all.

Source: Managed Futures = Barclayhedge CTA Index

Source: Managed Futures = Barclayhedge CTA Index

Of course, that’s the entire index – which by definition will be somewhat less volatile than its components. To dig into specific numbers and how managers approach these markets, there’s these four who ply their wares specifically in the energy space. There are these Ag managers in our featured collections, and this manager doing a type of metals arbitrage.

Ben says these strategies aren’t for the faint of heart, but we would argue that buying and holding commodities is not for the faint of heart, and a disciplined, systematic approach (be it his trend following model or via a professional) are the more conservative approach to commodity exposure.

The Managed Futures index is made up of hundreds and hundreds of managers with multiple programs which all have their own sets of the rules when it comes to making money in the markets, and a huge portion of that invested in financial futures, not just grown in the ground commodities. There are private funds, there are mutual funds, and soon to be more and more ETFs; each with their own benefit and drawbacks. This industry has been around for decades and becoming mainstream enough for more and more investors to consider, but maybe some rebranding is in order. Maybe the industry is better served talking about how it gives better commodity exposure than absolute returns or crisis period performance.

If you’re dedicated to having some commodity exposure, listen to Ben and avoid the long only commodity index products. But instead of becoming your own trend follower – needing to pay attention to when to get in and out – we would suggest taking a stroll through our new Managed Futures database with a complete list of all the managers who make up the Barclay hedge CTA database.

If there’s one thing we and Ben have in common when it comes to commodities – the trend is your friend.